Okay, picture this: You decide to make and sell custom-designed dog collars. Because, why not? Everyone loves dogs, and everyone loves dressing them up (even if the dogs themselves look perpetually embarrassed). You start small, working out of your garage. You get some materials, learn the basics of sewing (thanks, YouTube!), and boom! You’re in the dog collar business.

Demand starts picking up. Your friends love them, their friends love them, suddenly strangers are ordering online! You think, "This is it! I'm going to be the next big thing in canine couture!" So, you decide to expand. You need more space, more materials, maybe even hire a few helpers.

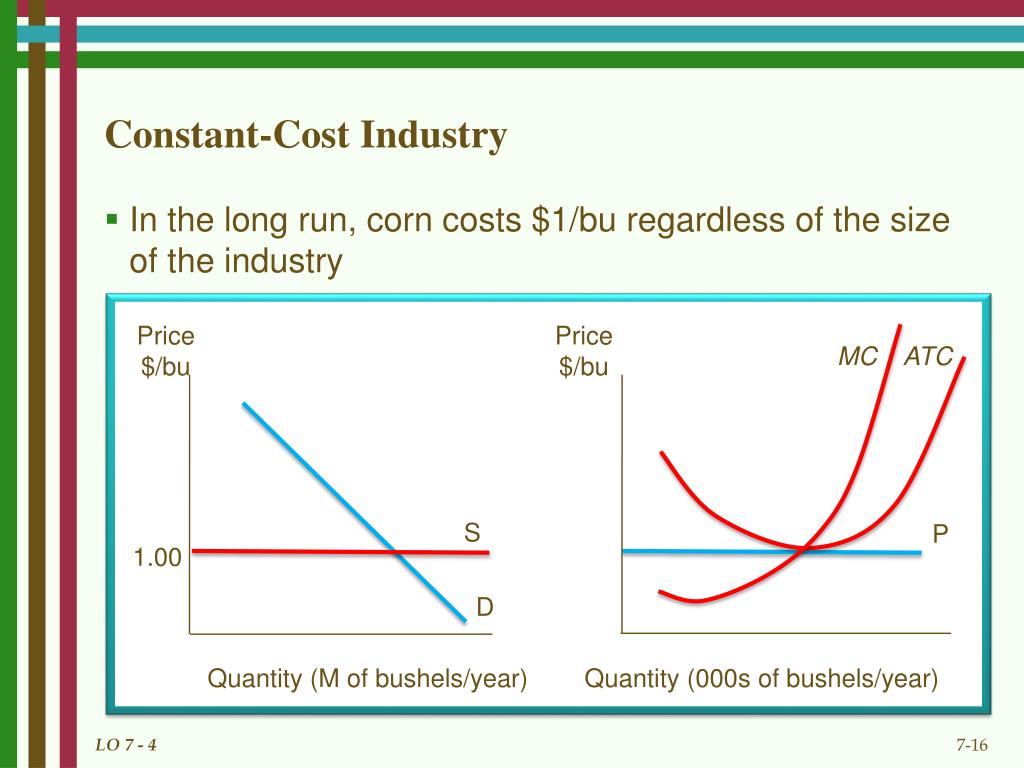

But here's the thing. As you grow, the price of the materials you need – the leather, the buckles, the thread – doesn't really change. You can buy more of it, and the suppliers don't suddenly jack up their prices just because you're buying in bulk. And the labor market? More or less the same hourly rate for skilled seamstresses. This, my friends, is a glimpse into the world of a constant cost industry.

What Exactly *Is* a Constant Cost Industry?

So, what does it mean if your hypothetical dog collar empire is operating in a constant cost industry? It means that as the industry as a whole expands (not just *your* business), the prices of the inputs (like materials and labor) used to make the product or service don't significantly increase. That’s the key. The cost of producing the good (or service) remains roughly the same, regardless of how much the industry produces.

Think of it this way: if a million more people suddenly wanted custom-designed dog collars, and everyone started opening up dog collar businesses, in a constant cost industry, the price of leather and buckles would likely stay relatively stable. (Famous last words, right? But bear with me!).

Why Does This Happen?

Several factors can contribute to an industry being classified as “constant cost”:

- Abundant Resources: The resources needed to produce the product are plentiful. There's no real shortage, even if demand increases dramatically. Think of something like… let’s say… generic white office paper. (Though even paper prices fluctuate sometimes, it’s generally a pretty stable resource).

- Highly Competitive Input Markets: The markets for the raw materials are already very competitive. Suppliers are already trying to keep prices low to attract customers, so a small increase in demand isn't enough to significantly drive up prices.

- Labor Availability: There is a large pool of readily available workers with the necessary skills. Expansion doesn't lead to wage increases because there are plenty of people who can do the job. (Of course, this is a simplification, and real-world labor markets are complex!).

The Supply Curve's Role

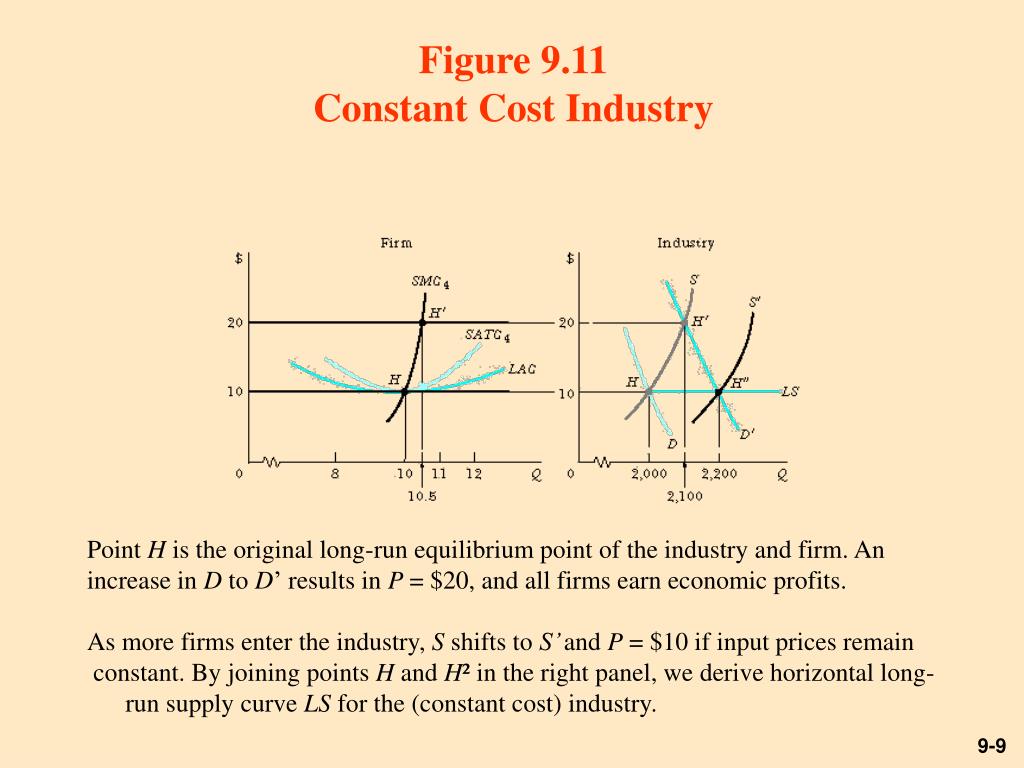

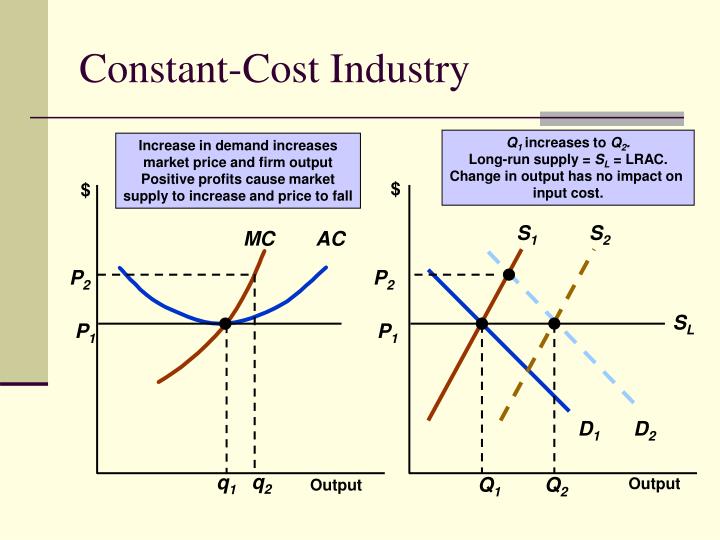

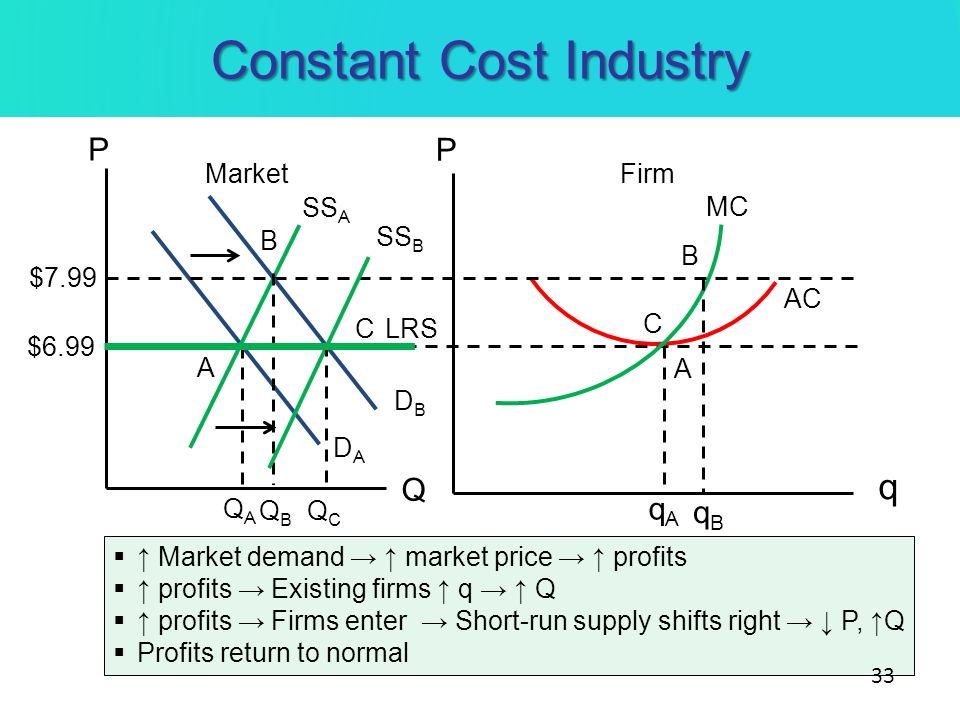

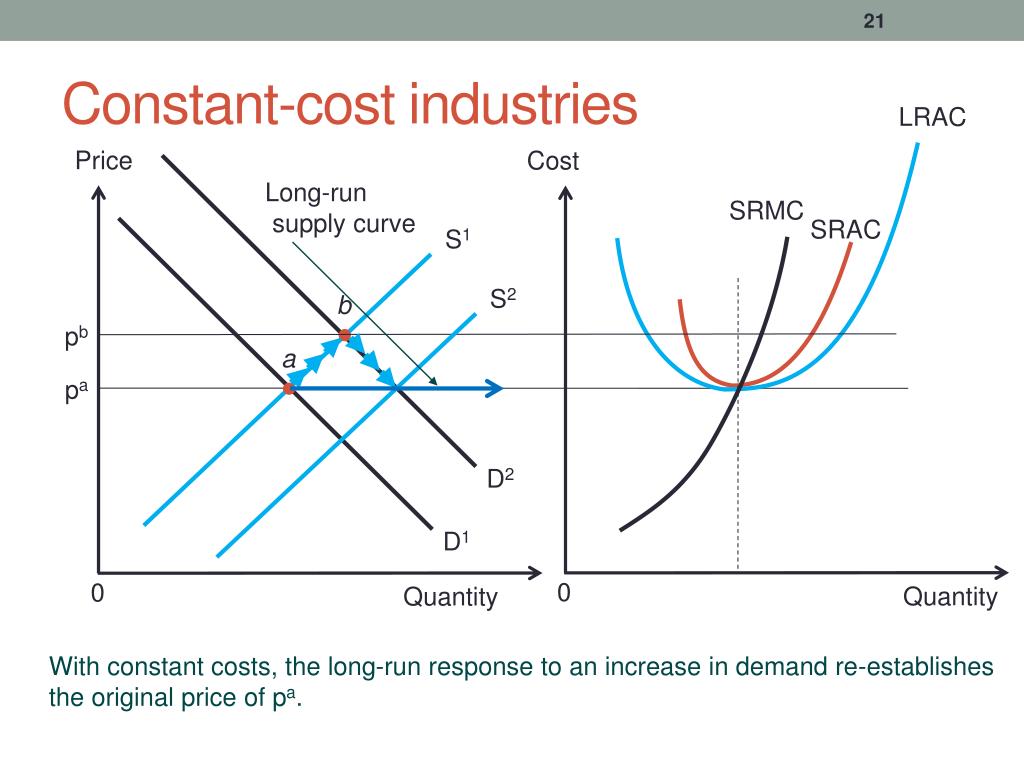

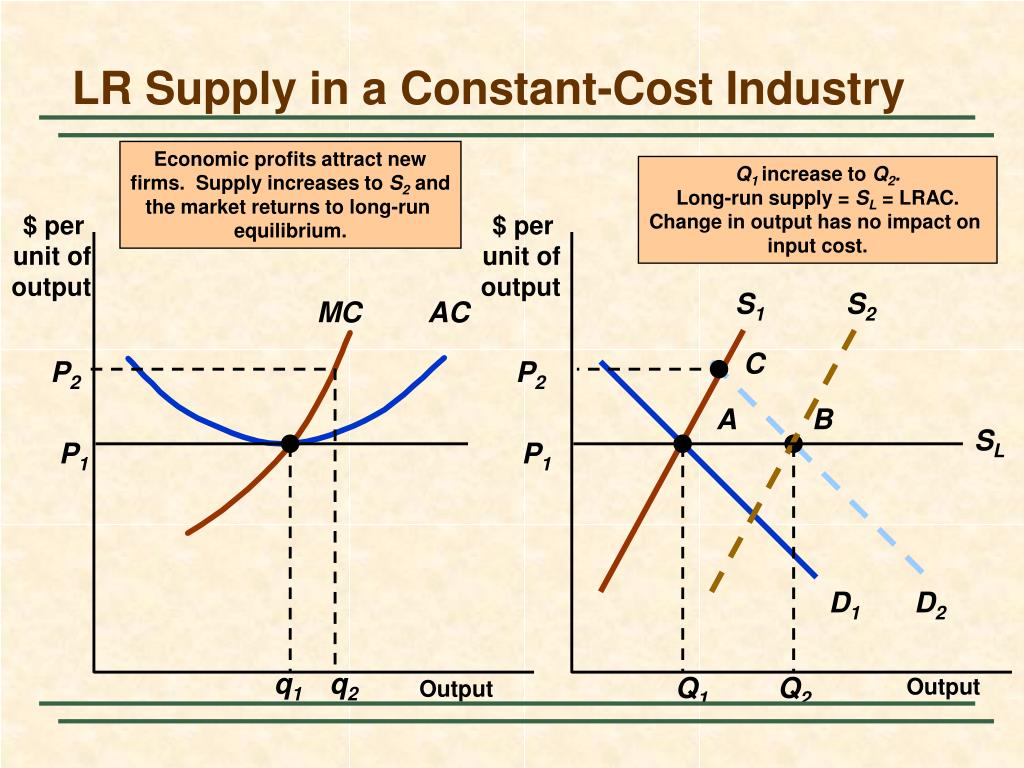

The defining characteristic of a constant cost industry is its long-run supply curve. It's a horizontal line. What does that mean? It means that the industry can supply any quantity of the good or service at the same price in the long run. Regardless of how much the demand increases, the long-run price will remain the same. Wild, isn’t it?

Let's break that down. Imagine a graph. The Y-axis is the price, and the X-axis is the quantity of dog collars produced. The supply curve in a constant cost industry is a straight, horizontal line across the graph. If demand for dog collars increases (the demand curve shifts to the right), the industry will produce more dog collars (we move along the X-axis), but the price (on the Y-axis) will remain the same. It just stays at the equilibrium price. No inflation there, folks.

Contrast This with Other Industries

To really understand constant cost industries, it's helpful to compare them to other types:

- Increasing Cost Industries: These are far more common. In these industries, as production increases, the cost of inputs rises, leading to higher prices for consumers. Think about the oil industry. As demand for oil increases, it becomes more expensive to extract (drilling deeper, exploring more remote locations), pushing up prices at the pump. The long-run supply curve slopes upward.

- Decreasing Cost Industries: These are rarer. As production increases, the cost of inputs *decreases*, leading to lower prices for consumers. This can happen when there are significant economies of scale. Think about the early days of computer manufacturing. As more computers were produced, the cost of components fell, and prices dropped. The long-run supply curve slopes downward.

Examples of Constant Cost Industries (Maybe!)

Finding *perfect* examples of constant cost industries in the real world is tricky. The economy is dynamic, and things are always changing. But some industries come closer than others.

- Certain Types of Manufacturing: Industries that rely on readily available, standardized materials (like certain types of plastic or commodity chemicals) might exhibit constant cost characteristics. If you need a million plastic forks, chances are the price per fork won't skyrocket just because you need so many.

- Some Service Industries: Certain services, like basic cleaning or landscaping, might be close to constant cost, especially if the labor market is competitive and there are many providers.

- Textile Production (Specific types): Depending on the specific type of fabric and the availability of raw materials, some textile production processes might approximate a constant cost scenario. Though, global events can always throw a wrench into that. (Remember the cotton price spike a few years back?!)

Important Caveat: It’s crucial to remember that this is a simplification. Even in these industries, there can be temporary fluctuations in prices due to factors like supply chain disruptions, changes in government regulations, or unexpected spikes in demand. But in the *long run*, the cost structure remains relatively stable.

Why Does This Matter? (Economic Implications)

Understanding constant cost industries is important for a few reasons:

- Predicting Price Changes: It helps economists and businesses predict how prices will react to changes in demand. If you're operating in a constant cost industry, you know that increasing production won't necessarily lead to higher prices (which is good news for consumers!).

- Policy Decisions: Governments need to understand industry cost structures when making policy decisions, such as setting taxes or regulations. Policies that might make sense in an increasing cost industry could have unintended consequences in a constant cost industry.

- Business Strategy: For businesses, knowing whether you're in a constant, increasing, or decreasing cost industry can inform your pricing strategy, investment decisions, and overall business plan. If you're confident that your input costs will remain stable, you might be more willing to invest in expanding your operations.

- Understanding Market Efficiency: Constant cost industries often indicate a high degree of market efficiency. The competition among suppliers and the availability of resources keep prices in check.

Back to the Dog Collars

Let's revisit our dog collar business. If you're operating in a true constant cost industry, you can confidently scale up your production without worrying too much about your input costs skyrocketing. You can focus on marketing, product development, and other aspects of your business, knowing that your cost structure is relatively stable. You could potentially flood the market with custom-designed dog collars! (Okay, maybe not *flood* the market. Over-saturation is a whole other problem!).

However, and this is a big however, you still need to keep an eye on things. Even in a constant cost industry, unexpected events can happen. A major supplier could go out of business, a new regulation could increase the cost of materials, or a sudden surge in demand could temporarily drive up prices. Vigilance is key, even when everything seems stable.

Final Thoughts

The concept of a constant cost industry is a useful theoretical framework for understanding how costs and prices interact in different markets. While perfect examples are rare, understanding the underlying principles can help you make better decisions as a consumer, a business owner, or an economist. And hey, if you *do* decide to start a dog collar business, now you’ll be much better prepared (economically speaking, at least). Just don't forget to factor in the cost of all those adorable puppy pictures you’ll inevitably take for marketing. Those are priceless!