Obtaining a $5,000 loan with a less-than-perfect credit score can be challenging, but it's certainly not impossible. While lenders typically prefer borrowers with excellent credit, various options are available for individuals seeking financing despite a history of credit challenges. This article explores these options and provides guidance on navigating the loan application process with bad credit.

Understanding the Landscape of Bad Credit Loans

Before delving into specific loan options, it's crucial to understand what constitutes "bad credit" and how it affects loan terms. Credit scores, typically ranging from 300 to 850, are numerical representations of your creditworthiness. Scores below 630 are generally considered "bad" or "poor," while scores between 630 and 689 are considered "fair."

A lower credit score signals a higher risk to lenders, often resulting in higher interest rates, stricter repayment terms, and potentially lower loan amounts. Lenders compensate for the increased risk by charging more interest and requiring collateral or a co-signer in some cases.

Factors Affecting Loan Approval with Bad Credit

Several factors beyond your credit score influence a lender's decision. These include:

- Income: A stable and sufficient income demonstrates your ability to repay the loan. Lenders will often request proof of income, such as pay stubs or bank statements.

- Debt-to-Income Ratio (DTI): This ratio compares your monthly debt payments to your gross monthly income. A lower DTI indicates a greater capacity to manage additional debt.

- Employment History: A consistent employment history signals stability and reduces the risk of job loss, which could impact your ability to repay the loan.

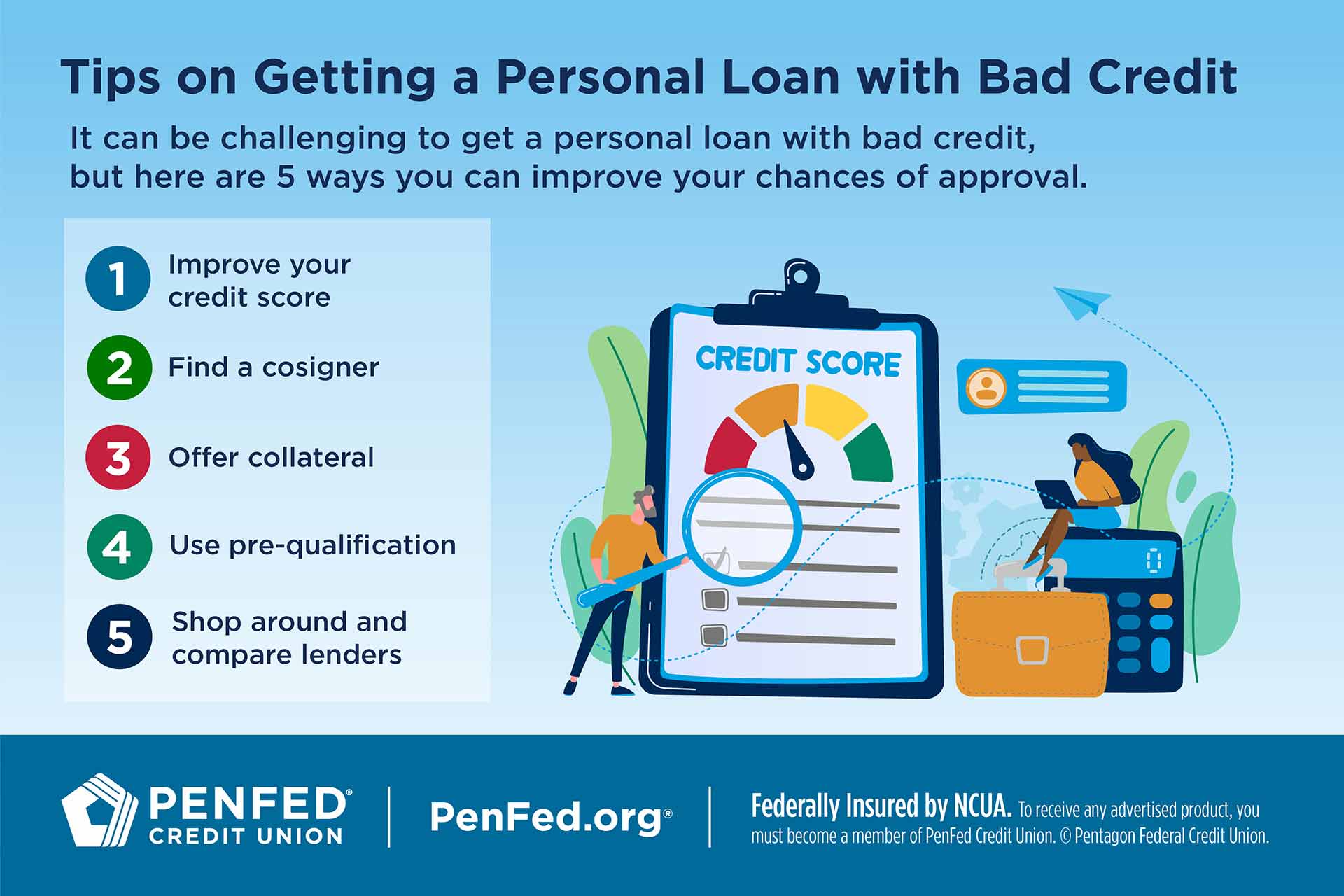

- Collateral: Offering collateral, such as a car or other asset, can secure the loan and reduce the lender's risk.

- Co-signer: A co-signer with good credit guarantees repayment if you default, making the loan less risky for the lender.

Loan Options for Borrowers with Bad Credit

Several loan options cater to individuals with credit challenges. Each option has its own advantages and disadvantages, so careful consideration is essential.

Personal Loans for Bad Credit

Several online lenders specialize in providing personal loans to borrowers with bad credit. These lenders often have more flexible eligibility criteria than traditional banks and credit unions.

Pros: Convenient online application process, potentially faster funding times, options available for various credit scores.

Cons: Higher interest rates compared to loans for borrowers with good credit, potential for fees (origination fees, prepayment penalties), loan amounts may be limited.

Secured Loans

Secured loans are backed by collateral, which reduces the lender's risk and can make it easier to qualify, even with bad credit. Common types of secured loans include auto loans and home equity loans.

Pros: Potentially lower interest rates than unsecured loans, higher loan amounts possible, easier to qualify for.

Cons: Risk of losing the collateral if you default on the loan, appraisal fees may be required, longer application process.

Credit Union Loans

Credit unions are non-profit financial institutions that often offer more favorable loan terms than traditional banks, especially for members with less-than-perfect credit. Membership is typically required.

Pros: Potentially lower interest rates and fees, more personalized service, community-focused lending practices.

Cons: Membership requirements, limited branch locations, loan amounts may be restricted.

Payday Loans and Title Loans (Proceed with Caution)

Payday loans and title loans are short-term, high-interest loans designed for emergency situations. They are generally not recommended for borrowers with bad credit due to their exorbitant interest rates and fees, which can trap borrowers in a cycle of debt.

Pros: Quick access to funds, minimal credit checks.

Cons: Extremely high interest rates and fees, short repayment terms, risk of losing your vehicle (with title loans). These loans should be considered a last resort.

Borrowing from Friends or Family

Borrowing from friends or family can be a viable option, especially if you have a strong relationship built on trust. However, it's crucial to formalize the loan agreement in writing to avoid misunderstandings and maintain healthy relationships.

Pros: Potentially lower interest rates or no interest at all, flexible repayment terms, less stringent eligibility requirements.

Cons: Potential for strained relationships if repayment issues arise, uncomfortable conversations about finances, can be difficult to maintain boundaries.

Improving Your Chances of Loan Approval

Regardless of the loan option you choose, there are steps you can take to improve your chances of approval and secure more favorable terms.

Check Your Credit Report

Obtain a copy of your credit report from each of the three major credit bureaus (Equifax, Experian, and TransUnion) and review them carefully for errors. Disputing and correcting errors can improve your credit score.

Lower Your Debt-to-Income Ratio

Reducing your outstanding debt can improve your DTI, making you a more attractive borrower. Consider paying down high-interest debt or consolidating debts into a single, lower-interest loan.

Provide Documentation

Gather all necessary documentation, such as proof of income, bank statements, and identification, to expedite the application process and demonstrate your ability to repay the loan.

Consider a Co-signer

If possible, find a creditworthy co-signer who is willing to guarantee repayment of the loan. This can significantly increase your chances of approval and potentially lower your interest rate.

Shop Around and Compare Offers

Don't settle for the first loan offer you receive. Shop around and compare offers from multiple lenders to find the most favorable terms. Pay attention to interest rates, fees, repayment terms, and loan amounts.

Protecting Yourself from Predatory Lenders

Be wary of lenders that offer guaranteed approval, charge excessive fees, or pressure you to take out a loan you can't afford. These may be predatory lenders who take advantage of vulnerable borrowers. Always read the fine print and understand the terms of the loan before signing any agreements.

Look for lenders that are transparent about their fees, interest rates, and repayment terms. Check their reputation with the Better Business Bureau and other consumer protection agencies.

Conclusion

Securing a $5,000 loan with bad credit requires careful planning, research, and a realistic understanding of your options. While interest rates may be higher and terms may be stricter, it is possible to obtain the financing you need by exploring different loan types, improving your creditworthiness, and shopping around for the best possible deal. Remember to prioritize responsible borrowing and avoid predatory lenders to protect your financial well-being.

The ability to access loans, even with less than perfect credit, is essential for individuals facing unexpected expenses, needing to consolidate debt, or pursuing opportunities for personal or professional growth. Understanding the options available and taking proactive steps to improve creditworthiness are crucial for navigating the financial landscape effectively.

/cloudfront-us-east-1.images.arcpublishing.com/dmn/VQTVMZKYXBBLVECIAWNZC46WME.jpg)