Okay, let's talk about something that might seem a little intimidating at first: getting a $5,000 loan when your credit isn't exactly sparkling. Don't worry! It's totally achievable, and you're definitely not alone. A lot of people are in the same boat. Think of this as a little adventure, a quest to financial empowerment! Ready? Let's dive in.

Why $5,000? And Why Should You Care?

First things first, why this specific amount? Five thousand dollars is a sweet spot. It's enough to tackle some serious needs – that overdue car repair (because, let's be real, cars always break down at the worst time!), a medical bill that’s been haunting you, maybe even a small home improvement project to finally fix that leaky faucet. Or maybe it’s about investing in *yourself* – a course to boost your skills, some equipment to start a side hustle…the possibilities are endless! It's about taking control and using that money to improve your life. Sounds good, right?

And why should you care about getting a loan, even with bad credit? Because it can be a powerful tool. It's about unlocking opportunities, relieving stress, and making progress towards your goals. Think of it as a stepping stone, not a life sentence.

Facing the Music: Understanding Your Credit Score

Alright, before we go any further, let's acknowledge the elephant in the room: your credit score. If you’ve got bad credit, it likely means you have a history of late payments, high credit card balances, or even a past bankruptcy. Don't beat yourself up about it! Everyone makes mistakes. The important thing is to learn from them and move forward.

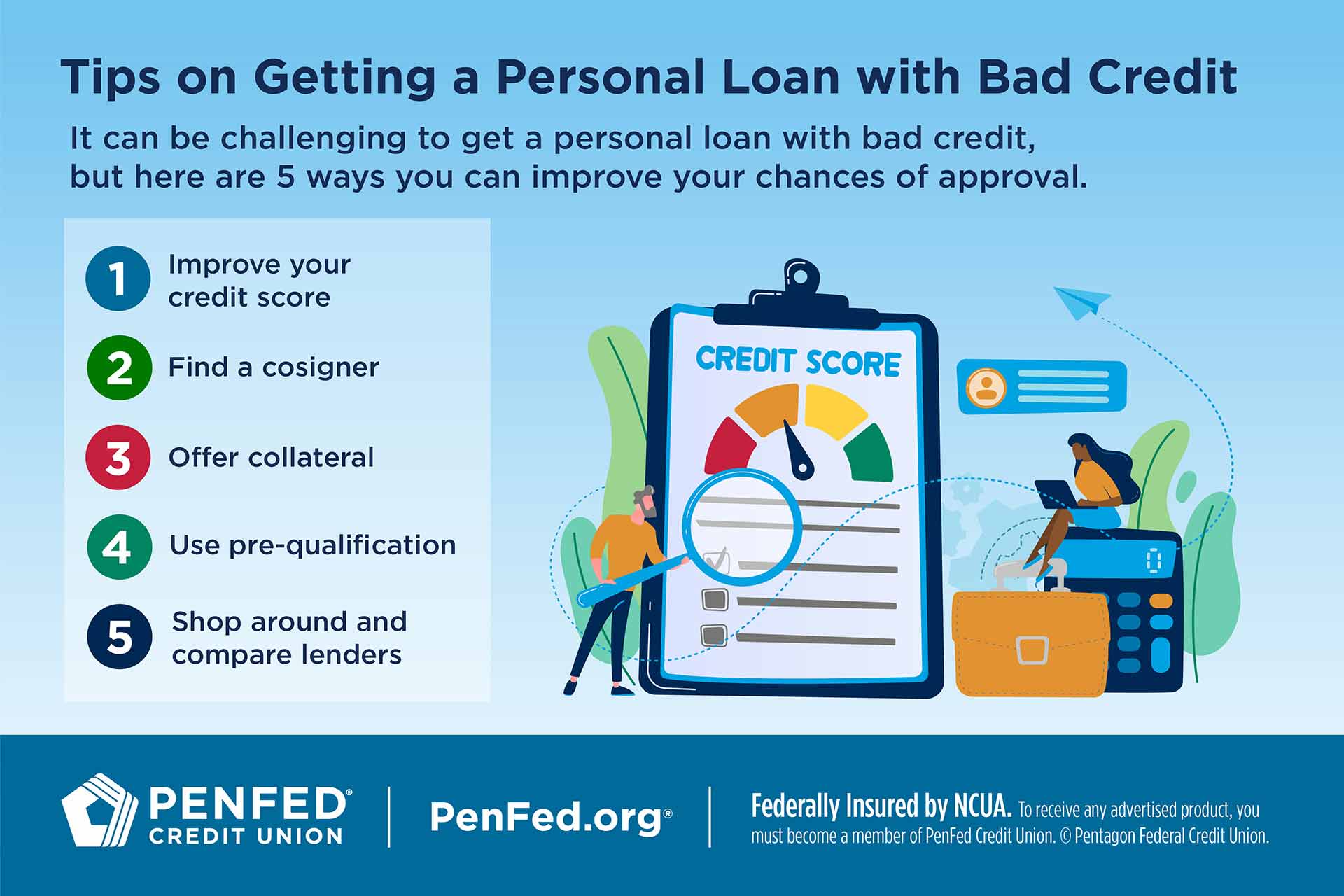

But, and this is a big but, knowing your credit score is crucial. It's like knowing your enemy in a video game. You can't beat it if you don't know its weaknesses! You can get your credit score for free from several websites, like Credit Karma or AnnualCreditReport.com. Take a look and see where you stand. This is the first step in the process. Don't be afraid, knowledge is power!

Understanding your credit report will show you what areas dragged your score down. Is it because of a specific missed payment? Maybe you have high balances on your credit cards. Addressing these issues can help improve your score over time. Which, as you'll see, helps you get better loan terms.

The Quest Begins: Exploring Your Loan Options

Now for the fun part: finding a loan! Don't assume you're stuck with exorbitant interest rates and predatory lenders. There are options out there, even with less-than-perfect credit. It just takes a little research and a proactive attitude.

Personal Loans for Bad Credit

These are specifically designed for people with lower credit scores. Lenders understand that life happens, and they're willing to take a chance. However, be prepared for higher interest rates and potentially some fees. It's the price you pay for the risk the lender is taking. But remember, it's often still better than doing nothing and letting your financial problems get worse!

Look for lenders who specialize in bad credit loans. Online lenders like Avant, Upgrade, and OneMain Financial are worth checking out. Compare their interest rates, terms, and fees carefully. Don't just jump at the first offer you see! It's like buying a car – you want to shop around for the best deal.

Secured Loans

This is where you put up something you own as collateral – like your car or maybe even your house (though be very careful about using your home!). Because the lender has something to seize if you don't repay the loan, they're more likely to approve you, even with bad credit. And often they will give you a lower interest rate!

However, this comes with risk. If you default on the loan, you could lose your collateral. So, be absolutely sure you can repay the loan before you take this option. It’s a powerful tool, but also a dangerous one if not used responsibly.

Credit Unions

Don't overlook your local credit unions! They're often more willing to work with members, especially those with less-than-perfect credit. They also tend to have lower interest rates and fees than traditional banks or online lenders. Plus, they’re community-focused. It’s always good to support local!

To join a credit union, you usually need to live, work, or worship in a specific area, or be affiliated with a particular organization. But once you're a member, you can access their loan products and other financial services. Definitely worth exploring!

Pawn Shops

Okay, this is more of a last resort. You bring in an item of value – jewelry, electronics, whatever – and they give you a short-term loan based on its value. If you don't repay the loan within the agreed-upon timeframe, they keep your item. Interest rates at pawn shops are typically very high, so it's best to avoid this option if possible. Think of it as a financial emergency button – use it sparingly!

Gear Up: Preparing Your Loan Application

Once you've identified a few potential lenders, it's time to prepare your loan application. This is where you show them you're serious and responsible, even if your credit history isn't perfect.

Gather Your Documents

You'll need to provide proof of income, such as pay stubs or tax returns. You'll also need to provide identification, such as a driver's license or passport. And you'll likely need to provide bank statements to show your financial history. The more organized you are, the better. It shows that you are detail-oriented and serious about your application!

Explain Your Situation

If you have a valid reason for your bad credit – like a job loss or a medical emergency – explain it in your application. Lenders are often more willing to work with borrowers who have faced unforeseen circumstances. Be honest and upfront. Lenders appreciate transparency!

Consider a Co-Signer

If you have a friend or family member with good credit who's willing to co-sign your loan, it can significantly increase your chances of approval. A co-signer essentially guarantees the loan, making the lender feel more secure. But be careful with this! If you don’t pay, the co-signer is responsible, and that can strain relationships. Only go this route if you're very confident in your ability to repay the loan.

Master the Negotiation: Getting the Best Terms

Don't just accept the first offer you get! Try to negotiate better terms. You might be surprised at what you can achieve. Remember, you’re the customer, and they want your business!

Shop Around

Get quotes from multiple lenders and compare them carefully. Use the best offer as leverage to negotiate with other lenders. "I got this rate from another lender, can you match it or beat it?" You'd be surprised how often they'll budge.

Negotiate the Interest Rate

Even a small reduction in the interest rate can save you a significant amount of money over the life of the loan. Be polite but persistent. Highlight your strengths as a borrower – like a stable job or a good repayment history on other loans. Remember, it never hurts to ask!

Negotiate the Fees

Some lenders charge origination fees, prepayment penalties, or other fees. Try to negotiate these fees down or eliminate them altogether. Ask questions like, "Is this fee negotiable?" or "Are there any ways to avoid this fee?"

The Aftermath: Responsible Loan Management

Congratulations! You got your $5,000 loan. But the journey doesn't end there. Now it's time to manage your loan responsibly and rebuild your credit.

Make On-Time Payments

This is the most important thing you can do. Set up automatic payments to ensure you never miss a due date. Late payments will only damage your credit further. Treat this loan payment like your lifeline. It can set you on a course for a much better financial future.

Avoid Taking on More Debt

Don't use your loan as an excuse to overspend. Stick to your budget and avoid taking on any new debt until you've repaid your loan. One step forward, two steps back is not what you want!

Monitor Your Credit Score

Keep an eye on your credit score and credit report. As you make on-time payments, your credit score should gradually improve. Celebrate your progress! It’s motivating to see those numbers rise.

Level Up: Rebuilding Your Credit

Getting a loan is just one step towards rebuilding your credit. Here are a few other things you can do:

Become an Authorized User

Ask a friend or family member with good credit to add you as an authorized user on their credit card. Their positive credit history will be reported to your credit report, helping to boost your score. Just make sure they are responsible with their card. You don’t want their bad habits hurting your score!

Get a Secured Credit Card

This is like a training wheels credit card. You deposit a certain amount of money as collateral, and that becomes your credit limit. As you use the card responsibly and make on-time payments, your credit score will improve. And, more importantly, it sets you on the path to positive credit management!

Dispute Errors on Your Credit Report

Sometimes, errors can appear on your credit report that are dragging down your score. Dispute these errors with the credit bureaus. They're legally obligated to investigate and correct any inaccuracies. It’s your right to have an accurate credit report!

The Grand Finale: Financial Freedom Awaits!

See? Getting a $5,000 loan with bad credit isn't impossible. It takes effort, research, and a willingness to learn. But it's totally achievable, and the rewards are well worth it.

By taking control of your finances, you can improve your credit score, unlock new opportunities, and achieve your financial goals. And isn't that what life is all about? Taking control and building the future you want? So, go out there, be proactive, and start your journey to financial freedom!

Now that you've got the basic knowledge to navigate the world of loans and credit repair, why not dive deeper? There are tons of resources online – free courses, articles, and communities of people who are on the same journey. Don't be afraid to explore and learn more. The more you know, the better equipped you'll be to make smart financial decisions. Good luck, and happy lending!